With the Nasdaq near all time highs, investor sentiment has never been more bullish towards US technology. However, with the Shiller P:E ratio hovering close to levels seen during the dot-com bubble, institutions are apprehensive whether this new AI wave is just another bubble waiting to implode. Michael Burry, the man who made millions shorting the housing market during the Global Financial Crisis, announced the closure of his fund due to several failed attempts to short the Nasdaq, stating he did not understand why these equities were trading at such crazy valuations. Ultimately, this got me thinking: are we in a bubble or are people just under-allocated?

Fundstrat Capital’s Tom Lee famously stated ‘when too many investors scream things are a bubble quite often they are sidelined,’ and this was the case in April when retail investors bought the Liberation Day dip on the Nasdaq whilst institutions remained sidelined until buying back stocks 10-20% higher. But now with the Nasdaq up 50% since, this should in theory mark a period of distribution with investors realising their profits, however with the Federal Reserve ending QT, consistent rate cuts and the labour market looking perilously weak it looks like there will be no shortage of stimulus in the economy. Hence, the question many have asked is how much longer can this continue until the bubble eventually bursts?

Betting on the Promise of a Better Tomorrow

The promise of the internet changing the world appealed to many investors in the 90s, and why wouldn’t it considering it was arguably the greatest human invention of all time. As humans we often get carried away by the promise of something often well before the fundamentals kick in. That greed is innate within us, we just can’t help it. And then once we run out of our own money we borrow money to invest or in this case bet on assets, since we are all in unison that things will never come down. And that’s when the bubble bursts. One of the main reasons for the Wall Street Crash in 1929 was the buildup of excessive leverage in the system due to bets being made on assets which everyone thought would make them rich. And at the time it could be argued the investors were right, since advancements were being made in technology and manufacturing with the demand for those sectors only increasing during the mid to late 1920s. However, these bets were made using loans from banks because investors in their euphoria never believed the banks would collapse, once again betting on the promise of a better tomorrow. During periods of euphoria, humans feel like they are invincible and they aren’t satisfied with realising their profits because they feel like they will miss out on more. Nonetheless, whatever goes up must go down and this sentiment was eerily similar during the dot-com bubble mania where investors were piling in on their long bets towards assets which had no fundamentals or numbers backing up the prospect of future growth.

Were they just early?

In my honest belief, investors are usually just early to ‘era-defining trades’ because the fundamentals take a while but they do eventually catch up. When the dot-com bubble burst most companies that paid for all this went bankrupt, but the infrastructure remained. This allowed the engineers to work on the physical infrastructure of the internet where the fiber-optic networks, data centers, servers, and broadband rollout created in that period became the bedrock on which every successful tech company of the 2000s and 2010s was built. Today’s breakthroughs in AI, cloud computing, biotech, robotics—aren’t floating on hype alone; they run on infrastructure that’s been tried and tested for decades. But, it is also something that is in a constant state of evolution. The lesson from the dot-com bubble isn’t that tech manias are dangerous, it’s that once the foundations are laid; real innovation can finally flow.

Global Adoption of the Internet

In the late 90s, 5% of the world’s population had access to the internet so the demand for technology wasn’t on a worldwide scale. Now with more than 6 billion people using the internet and with almost 1 billion using tools like ChatGPT as a resource for their knowledge. The infrastructure demand for data centers, GPUs and computational power is rising in a way that creates durable capital spending. Financial markets are ultimately a reflection of human behaviour. Stock prices don’t move in a vacuum but they respond to how people live, work, communicate, and solve problems every day. When a technology becomes woven into daily routines, from how businesses operate to how individuals shop, learn, or entertain themselves, the market simply mirrors that rising demand. That’s why today’s tech boom is different from past bubbles: the products aren’t speculative promises of the future, they’re tools billions of people already rely on. Markets aren’t pricing hope they’re pricing in our material needs which need to be fulfilled because the future usage and demand for technology will only increase.

The Tech Giants

Critics often point to the dominance of the Magnificent Seven which is now nearly 40% of the Nasdaq’s total market capitalisation, as evidence that markets have become dangerously concentrated. But, in my eyes this concentration is arguably a sign of strength and not fragility. Investors aren’t blindly speculating on unproven startups the way they did during the dot-com era; they’re allocating capital to some of the most profitable and technologically advanced companies in human history. These firms have already demonstrated their ability to scale globally, generate consistent earnings, and reinvest billions into the infrastructure powering AI, cloud computing, and semiconductors.

Just this past week, Nvidia released their earnings report where they once again resoundingly beat expectations by printing revenues of $57 billion up 60% on the year with their EPS of $1.30 up 0.78 in the same timespan. Jensen Huang said, ‘their cloud GPUs were sold out’ and rejected fears of an AI bubble saying that ‘their data shows them something completely different’. And why would we not believe him, his company has been at the heart of the AI revolution and even with their current market capitalisation at $5 trillion, they’re still growing at a rate of 60% a year with jaw-dropping numbers backing their valuation. But it wasn’t just Nvidia, most of the Mag7 beat their revenue estimates in their latest financial reports and with the United States locked in an accelerating technological arms race with China, investment flows into these giants are unlikely to slow. Washington and Wall Street both recognise that leadership in AI, chips, and advanced computing is now a matter of national competitiveness, ensuring that the Mag7 continue to attract capital not because of hype, but because they are the backbone of America’s technological defence.

Crypto’s Weakness: Is it a Bubble?

However, amongst all the tech mania that has occurred this year, Bitcoin is down 5% on the year which has been an aberration from other bull market cycles. The Crypto market has lagged the stock market significantly making it a painful time for investors holding assets well outside the risk curve whilst not getting their risk-adjusted returns.

Jordi Visser wrote an article outlining how Bitcoin is going through its ‘silent IPO moment’, where the early Bitcoin whales are selling their Bitcoin to tradfi institutions, especially now that the asset can withstand the billions of dollars being dumped on the market. He argues that this wealth transfer is a launchpad for the future growth of Bitcoin because institutions are now the new long-term buyers for the asset and will continue accumulating at cheaper prices with the intention to hold for decades unlike the average retailer. Ultimately, there’s a lot of truth to this thesis as Bitcoin has become more institutionalised ever since its ETF launch and has been trading more like a macro asset with decreasing levels of volatility relative to its pre-ETF days. Whilst Bitcoin has maintained price stability on the year other Cryptocurrencies have gone through periods of extensive volatility to the downside, with Solana, Ethereum and XRP just to name a few all down on the year and unable to push to sustain new highs.

However, my belief is that Bitcoin’s underperformance relative to the Nasdaq has very little to do with the bearish factors in the wider Crypto market and unlike in tech stocks, we are seeing the aftermath of Crypto’s very own mini dot-com bubble implosion, which began on January 17th 2025. Trump’s memecoin launch sparked retail mania in the market, with the token going from a few billion to 70 billion in a matter of days causing Solana to pump to $300 and various other memecoins made new highs within a span of 48 hours. Trump had many crypto millionaires in a matter of minutes, but left an indelible mark on the space where investors are still reeling from the fallout of the bloodbath that followed. Not so soon after $Trump was released, his team launched the $Melania token which meant that the retail investors who FOMO’d in on the tops of the Trump coin launch were the exit liquidity. Ever since then, neither tokens have revisited their highs and retail has refrained from re-entering the market.

The memecoin mania which was the narrative of 2024, and what had started off as a way of communities coming together and making a meme ‘investable’ had now become the ultimate zero-sum game.

That week of January 17th, the bubble had burst, but there wasn’t a sudden downturn in price; it was a slow and dreadful bleed to the lows. The wider Crypto market had lost its way and many realised the altcoin space was a mere speculative bubble not driven by fundamentals or real-world value, but entirely by speculation. The final nail was the October 10th liquidation event which showed the thin order books for the wider asset class and how price is driven more so by manipulation through perpetual trading than it is by longer-term spot buying.

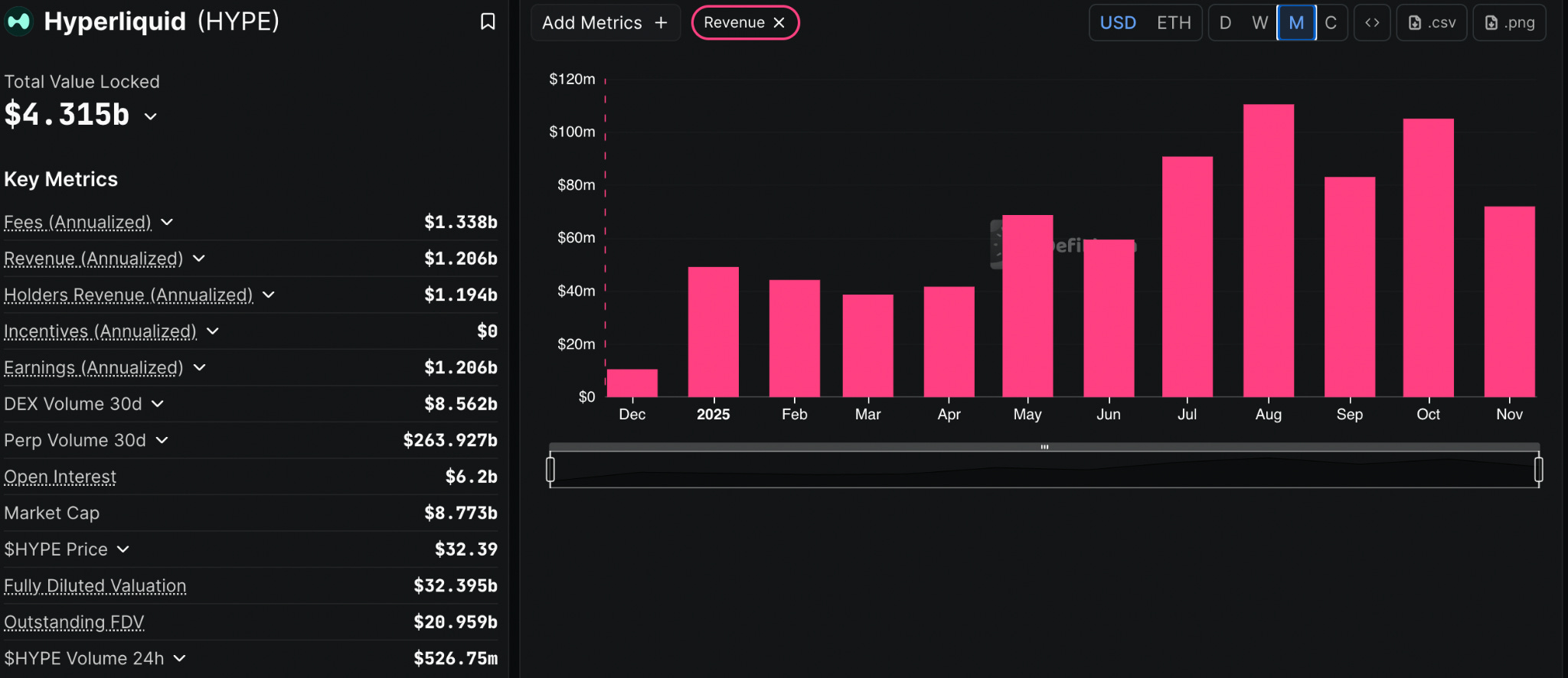

Hyperliquid: A Sign of Better Times to Come

The only token in the Top 15 Crypto assets besides Zcash’s recent explosion to be positive on the year is Hyperliquid. The HYPE token is up 50% on the year and has firmly established its dominance in the DeFi space as the leading perpetual decentralised exchange. One of the reasons why it has outperformed the overall market is because of its product market fit and buyback mechanism. Jeff, the founder of Hyperliquid, had managed to create a transformative product that would onboard users whilst rewarding them with token buybacks from its revenue as a way of incentivising the use of the DEX. Hyperliquid’s revolution has now changed the altcoin landscape and now more and more Crypto projects are adopting its approach for success, because they have realised the game has changed. Vaporware crypto projects have no space in the market anymore; to survive, you must provide value or else risk being cast away. Following the burst of the dot-com bubble, tech entrepreneurs realised that to receive venture capitalist funding, their projects needed to create demand in the market. Similarly, Crypto is going through its period of maturity. Hyperliquid has shown how to thrive in a period of weakness, however this must continue; January 17th had burst the bubble but was that a blessing in the long-term only time will tell.

( DefiLlama’s Hyperliquid Revenue chart)

Final Thoughts

Human innovation compounds with every generation, and the tech revolution is the clearest expression of that progress. Artificial Intelligence is now so deeply embedded in daily life that a true “bubble burst” would require people to stop using it entirely. Comparing today to the dot-com era misses this simple truth: back then, few even understood the internet, while now advanced technology operates in milliseconds at global scale. Calling every period of outperformance a bubble ignores the role of adoption, maturity, and real economic utility. That is not to say markets are not unforgiving as soon as there’s signs of euphoria they will correct as we have seen in the Crypto markets this year, but also during April of this year where all markets unwound the buildup of leverage in the system; that’s a sign of a healthy market reset. But, what I can’t foresee is a fundamental collapse of US technology at least not for now, but I guess with time we shall find out.